CattleFax Forecasts Record Beef Demand; Prospects for Tighter Supplies

August 11, 2021

The beef cattle industry is bouncing back from the pandemic, and continued progress is expected in 2022. Beef prices are near record high, and consumer and wholesale beef demand are both at 30-year highs as the U.S. and global economy recover. While drought remains a significant concern with weather threatening pasture conditions in the Northern Plains and West, strong demand, combined with higher cattle prices, signal an optimistic future for the beef industry, according to CattleFax. The popular CattleFax Outlook Seminar, held as part of the 2021 Cattle Industry Convention and NCBA Trade Show in Nashville, shared expert market and weather analysis today.

According to CattleFax CEO Randy Blach, the cattle market is still dealing with a burdensome supply of market-ready fed cattle. The influence of that supply will diminish as three years of herd liquidation will reduce feedyard placements. As this occurs, the value of calves, feeder cattle and fed cattle will increase several hundred dollars per head over the next few years.

Kevin Good, vice president of industry relations and analysis at CattleFax, reported that the most recent cattle cycle saw cattle inventories peak at 94.8 million head and that those numbers are still in the system due to the COVID-19 induced slowdown in harvest over the past year.

“As drought, market volatility and processing capacity challenges unnerved producers over the past 24 months, the industry is liquidating the beef cowherd which is expected to decline 400,000 head by Jan. 1 reaching 30.7 million head,” Good said.

The feeder cattle and calf supply will decline roughly 1 million head from its peak during this contraction phase. Fed cattle slaughter will remain larger through 2021 as carryover from pandemic disruptions works through a processing segment hindered by labor issues, he added.

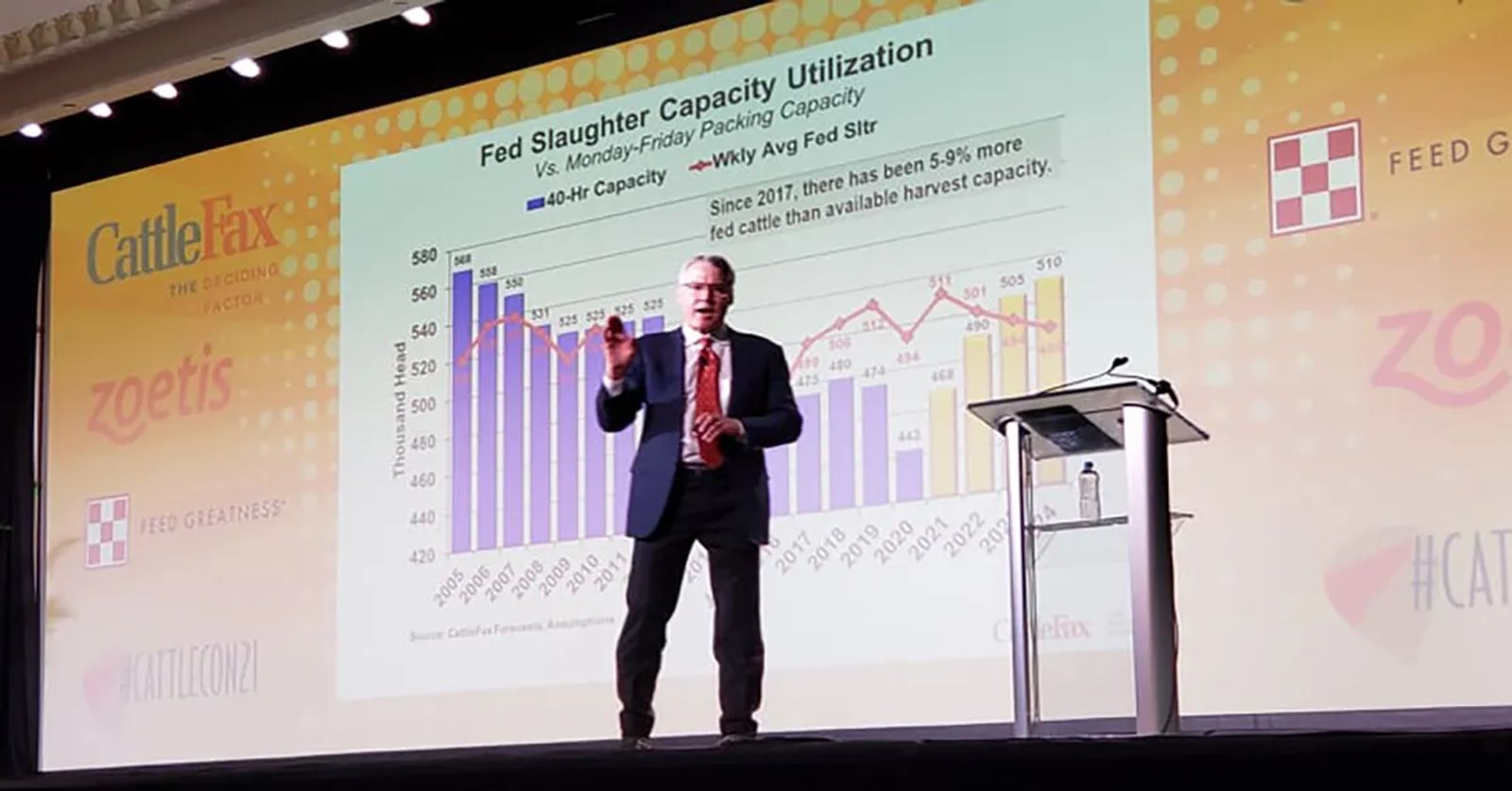

“While fed cattle slaughter nearly equals 2019 highs at 26.5 million head this year, we expect a 500,000-head decline in 2022,” Good said. “This, combined with plans for new packing plants and expansions possibly adding near 25,000 head per week of slaughter capacity over the next few years, should restore leverage back to the producer.”

Good forecasted the average 2022 fed steer price at $135/cwt., up $14/cwt. from 2021, with a range of $120 to $150/cwt. throughout the year. All cattle classes are expected to trade higher, and prices are expected to improve over the next three years. The 800-lb. steer price is expected to average $165/cwt. with a range of $150 to $180/cwt., and the 550-lb. steer price is expected to average $200/cwt., with a range of $170 to $230/cwt. Finally, Good forecasted utility cows at an average of $70/cwt. with a range of $60 to $80/cwt., and bred cows at an average of $1,750/cwt. with a range of $1,600 to $1,900 for load lots of quality, running-age cows.

Consumer demand for beef at home and around the globe remained strong in 2021, a trend that will continue in 2022, especially as tight global protein supplies are expected to fuel U.S. export growth.

Aftershocks from the pandemic continue to keep domestic demand at elevated levels not seen since 1988. Government stimulus and unemployment benefits are fueling the economy with demand outpacing available supplies as restaurants and entertainment segments emerge from shutdowns.

According to Good, the boxed beef cutout peaked at $336/cwt. in June, while retail beef prices pushed to annual high at $7.11/lb. “Customer traffic remained strong at restaurants and retail – even as those segments pushed on the higher costs, proving consumers are willing to pay more for beef,” he said.

Wholesale demand will be softer in 2022, as a bigger decline in beef supplies will offset a smaller increase in beef prices with the cutout expected to increase $5 to $265/cwt. Retailers and restaurants continue to adjust prices higher to cover costs. Good added the retail beef prices are expected to average $6.80/lb. in 2021 and increase to $6.85/lb. in 2022.

Global protein demand has increased and U.S. beef exports have posted new record highs for two consecutive months, even with high wholesale prices. The increases were led by large, year-over-year gains into China, and Japan and South Korea remaining strong trade partners for protein. “The tightening of global protein supplies will support stronger U.S. red meat exports in 2022. U.S. beef exports are expected to grow 15 percent in 2021 and another 5 percent in 2022,” Good said.

Mike Murphy, CattleFax vice president of research and risk management services, expects summer weather patterns – and their affect on corn and soybean yields – to be the focus of market participants.

“As China rebuilds its pork industry following their battle with African Swine Fever, they are looking for higher quality feed ingredients, such as corn and soybeans” Murphy said “Exceptional demand from China is leading U.S. corn exports to a new record in the current market year, and strong demand for U.S. soybeans has elevated prices in the last 12 months.”

Spot prices for soybeans are expected to be $13 to $16 per bushel for the remainder of the next 18 months along with spot corn futures to trade between $4.75 to $6.25 per bushel in the same time frame.

Murphy noted that drier weather in the Northern Plains and West will pressure hay production and quality in the 2021 season – supporting prices into the next year. “May 1 on-farm hay stocks were down 12 percent from the previous year, at 18 million tons. The USDA estimates hay acres are down 700,000 from last year at 51.5 million acres. So, expect current year hay prices to average near $170/ton, and 2022 average prices should be steady to $10 higher due to tighter supplies and stronger demand,” he said.

All session panelists agreed that weather is a major factor impacting the beef industry, and agriculture as a whole in 2021 and going into 2022. A forecasted return of La Niña this fall would lead to intensifying drought for the West and Plains into early 2022, according to Dr. Art Douglas, professor emeritus at Creighton University. Douglas indicated that the precipitation outlook in the fall of 2021 going into the early part of 2022 could see drought push harder in the Pacific Northwest with above-normal precipitation across the inter-mountain West – leaving the Midwest drier, and less tropical storm activity to reduce Southeast rainfall into late fall. Also, the western half of the country will be drier into early spring with a returning La Nina.

Blach concluded the session with an overall positive outlook, expecting margins to improve as cattle supply tightens and producers gain leverage back from packers and retailers, beef demand to remain solid with expected export growth, and utilization and packing capacity to improve over the next few years. He also noted that the economy has made gains in 2021 and should stay stronger with low interest rates and government stimulus fueling consumer spending.

Source: NCBA, Western Ag Network