A (Potentially) BIG DAY for Grains

May 23, 2023 - After a long winter, it may be hard to believe, but it is time for USDA's May WASDE and Crop Production reports, two reports with lots of estimates for the new season ahead, as well as updates for the current 2022-23 season. Both reports will be released at 11 a.m. CDT on Friday, May 12, followed with prompt coverage by DTN and a free DTN webinar at 12:30 p.m.

CORN

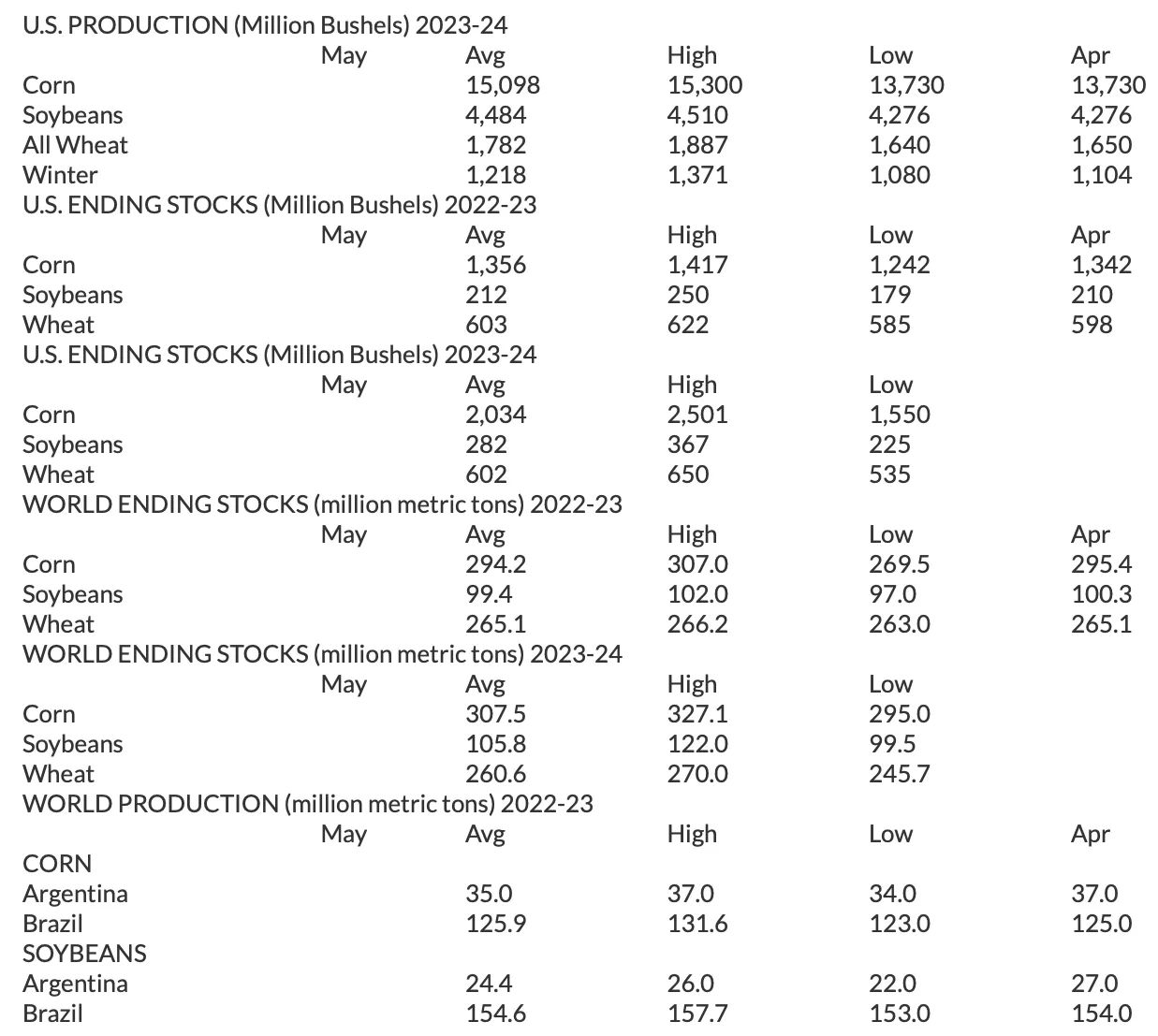

For much of 2022-23, we've talked about old-crop corn supplies being lower than usual, supporting corn prices above $6 per bushel. However, July corn is now below $6.00 and slipping as prices encounter pressure from the anticipation of a big crop in Brazil and a poor pace of U.S. export sales. Dow Jones' survey of 20 analysts expects USDA to raise its estimate of U.S. old-crop ending corn stocks from 1.342 billion bushels (bb) in April to 1.356 bb in May, a number that has room to go higher if USDA sees fit.

For the new 2023-24 season, Dow Jones expects USDA to estimate U.S. ending corn stocks at 2.034 bb, based on harvesting a 15.098 bb crop in the fall. If true, it would be the second largest crop on record and the largest ending corn stocks in five years. With North Dakota only 1% planted as of May 7, we still don't know if 92.0 million acres of corn plantings are possible and my personal estimate stays at 90.0 million acres for now. If the U.S. experiences the good weather scenario that DTN's weather team expects for 2023, there will be room for corn's ending stocks estimate to build even higher.

Outside of the U.S., Dow Jones' survey expects a slightly higher corn production estimate for Brazil, to a record-high 125.9 million metric tons (mmt) or 4.96 bb. Argentina's production estimate is expected to drop from 37.0 mmt in April to 35.0 mmt in May or 1.38 bb, the lowest in five years. USDA's estimate of world ending corn stocks in 2022-23 is expected to slip from 295.35 mmt in April to 294.2 mmt or 11.58 bb on Friday. The 2023-24 estimate of world ending corn stocks is too early to take seriously but is expected at 307.5 mmt or 12.11 bb. The more important world metric to watch for 2022-23 is the estimate of world ending corn stocks, excluding China, last seen at 88.03 mmt or 3.47 bb, the second lowest in 10 years.

SOYBEANS

Old-crop soybean prices have also been slipping lower the past two months, but Dow Jones' survey does not see much change in supplies. The survey expects USDA to increase its estimate of U.S. ending soybean stocks in 2022-23 from 210 million bushels (mb) to 212 mb. If true, it will still be the lowest ending supplies in seven years and will hardly be noticed by traders. At this point, it is difficult to disagree with the survey, but by the end of the season, we may see that summer demand slowed more than expected to accommodate the limited amount of supplies available.

For the new 2023-24 season, Dow Jones expects U.S. ending soybean stocks to climb to 282 mb, the highest in four years, based on a record-high 4.484 bb crop this fall. As with corn, weather will have the largest say and DTN's current forecast for August looks especially promising for soybeans with a large coverage of rain expected. So far, soybean planting is off to a good start and has time for higher temperatures to help northern states catch up.

Dow Jones' expects USDA's estimate of world soybean stocks to slip from 100.29 mmt to 99.4 mmt or 3.65 bb in 2022-23, not much of a change. The production estimate for Brazil is expected slightly higher, at 154.6 mmt or 5.68 bb. Argentina's production estimate is expected to drop from 27.0 mmt in April to 24.4 mmt or 897 mb on Friday, the lowest in 23 years. Similar to corn, USDA's estimate of world soybean stocks in 2023-24 won't carry a lot of weight this early but supports a bearish outlook. Dow Jones' survey is expecting a higher estimate of 105.8 mmt or 3.89 bb.

WHEAT

With the start of a new wheat season less than a month away in the Northern Hemisphere, Dow Jones' survey expects an old-crop estimate of 265.1 mmt or 9.74 bb of world ending wheat stocks to transition to a modestly lower, new-crop world estimate of 260.6 mmt or 9.58 bb. As with corn, the more interesting metric will be USDA's estimate of world ending wheat stocks, excluding China, last seen at 125.47 mmt or 4.61 bb in 2022-23, the lowest total in 14 years. There will also be early interest in new-crop production estimates of the world's major growers.

For the U.S., Dow Jones' expects a slight increase in old-crop ending stocks, from 598 mb in April to 603 mb in May, still the lowest in nine years. For the new season, Dow Jones' expects ending U.S. wheat stocks to stay virtually unchanged at 602 mb, but have higher wheat production of 1.782 bb. Given this year's problems with drought in the southwestern Plains and planting hurdles for spring wheat, I can't predict what USDA will say, but suspect U.S. wheat production will eventually come in closer to last year's 1.650 bb.

Looking at the Crop Production report from NASS, Dow Jones' estimates 1.218 bb of winter wheat production, parsed out as 588 mb of hard red, 397 mb of soft red and 238 mb of white wheat. With 68% of Kansas wheat given a poor to very poor rating as of May 7, the lowest for that date since 1989, I'll take the under on the hard red estimate.

For Friday's new-crop estimates especially, Dow Jones' surveys come with wide ranges of guesses, pointing out both, the level of difficulty in looking ahead as well as high degrees of uncertainty -- an environment ripe for surprises. I can't promise Friday's new USDA estimates will be accurate, but May reports are always interesting and make for good conversation.

Join DTN's webinar at 12:30 p.m. CDT on Friday, May 12, as we go through the numbers, explain what they mean for prices and hear my views on which estimates are reasonable and which are not. We also invite and make time for questions. Register here for Friday's May WASDE and Crop Production reports webinar.

Source: DTN, Todd Hultman