Meat Snack Boom

June 2, 2026

Eating behavior has evolved rapidly in recent years. Consumers are increasingly drawn to foods that are minimally processed, high in protein, nutritious and offer convenience and value. Nearly all of these attributes have boosted meat snack offerings with a 45% jump in meat snack sales over the past four years. The meat snack space is primarily dominated by beef-derived items such as beef jerky or sticks. However, innovative options utilizing pork, poultry or exotic meats have gained market presence. This space is far from static and easily adapts to changing consumer preferences.

Increasing popularity of meat snack items has spurred investment in further processing in recent years. While the majority of focus has been on beef items, competing meats are latching on to that success, albeit less intensely. And although we expect beef will remain king, comparative pork and poultry offering opportunities should not be dismissed.

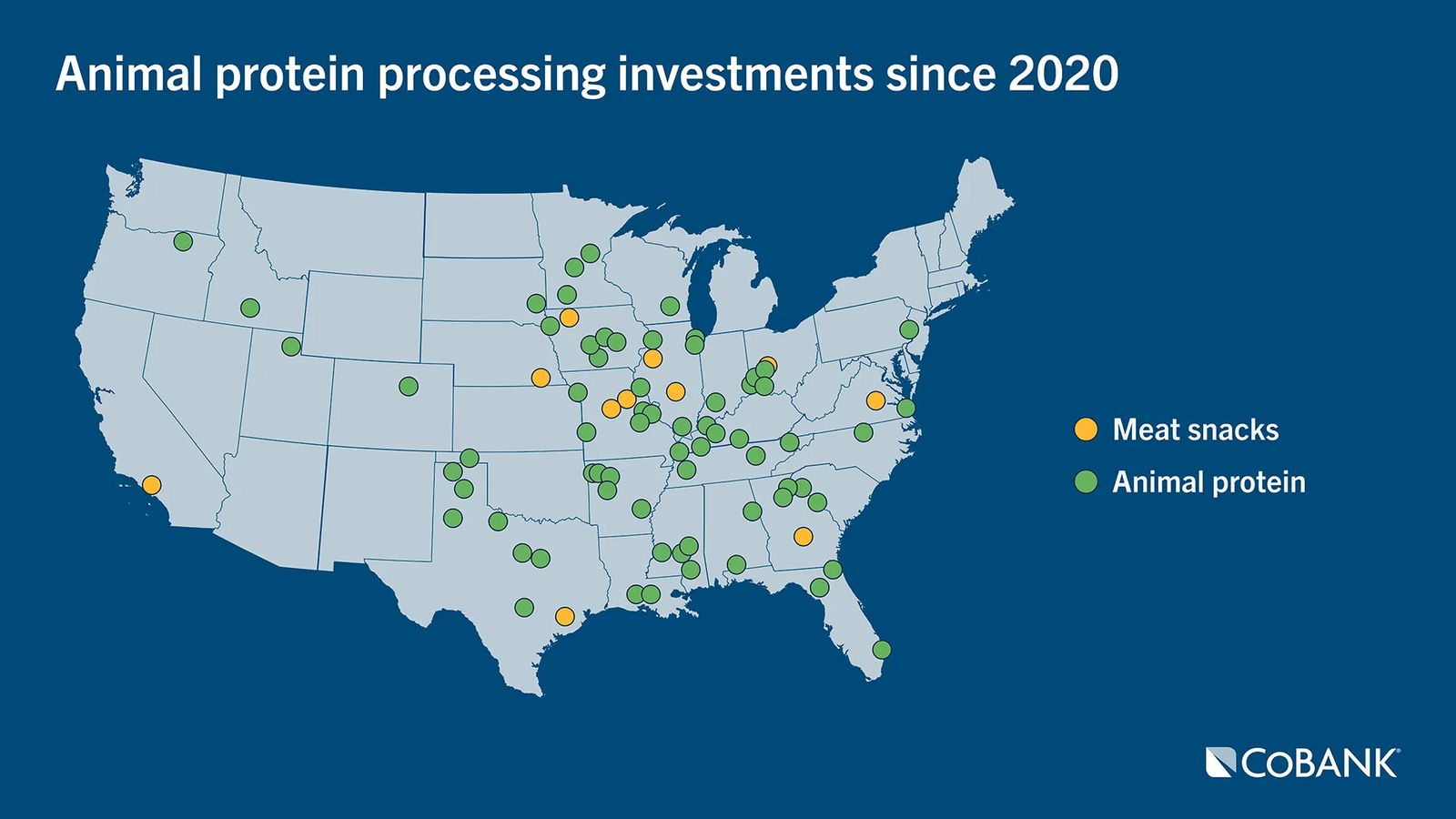

Processing investment taking place across the country

In step with increased consumer preference for meat snacks, capital expenditures have been significant in recent years. More than $1 billion of additional processing investment for meat snacks has been announced since 2020. This compares to a total of $8 billion invested for all animal processing (including primary processing and other further processing capacity). Notably, in 2025, several plants opened or announced construction across the country, including investments from popular brands like Chomps, Jack Link’s, and Archers. Jack Link’s, for example, announced a $450 million investment for a new plant in Perry, Georgia, aimed at expanding its processing capabilities. Chomps is building two manufacturing facilities in Missouri and Nebraska to double its meat snack production this year.

Source: Meat+Poultry, Swine Web, Food Business News, The National Provisioner

Competition for raw material seen as a growth constraint

When thinking about the meat snack landscape, an important structural issue of beef jerky production is the cattle cycle itself. The U.S. herd has fallen to its lowest level since the 1950s after drought and high feed costs triggered liquidation. That has especially tightened supply of lean beef for further processing, beef from retired cows, and end meats like rounds and chucks.

Another factor tightening beef supplies for further processing is exceptionally strong demand. The beef jerky market has had difficulty rationalizing these two forces. Beef jerky production shares raw material sourcing with ground beef, and at times, end cuts that may be sold as roasts.

Throughout seasonal cycles, some beef end cuts — rounds (eye, top, inside, bottom), knuckles and sirloin tips — may have difficulty clearing through retail or food service outlets in whole muscle form. At that point, the market diverts these items to further processing.

That matters because jerky manufacturers compete directly with hamburger grinders, foodservice, deli roast beef processors, export buyers, and value-added cooked beef manufacturers. The wholesale data reflects this pressure. The prices for most roasts rose 20% or more YoY to start 2025 and have remained persistently higher in 2026.

For jerky producers, these higher costs have created a real squeeze. Raw material inflation is on top of yield loss when compared with the economics of ground beef. Whereas lean ground beef can be upgraded by adding fat content, fat is less desirable in jerky and yield goes in the opposite direction. Producing 1 pound of finished jerky takes roughly 2.5–3.5 pounds of raw beef, so when lean round prices jump, finished jerky costs move sharply higher.

The opportunity has never been stronger for other animal proteins

With constrained beef availability due to a contracting herd size, the opportunity is rising for pork and poultry to offer value-oriented alternatives.

For years, pork has struggled to gain domestic market share for its traditional offerings. U.S. pork consumption has stagnated at an average of 50 pounds per capita annually. However, companies are experimenting with products like ready-to-eat bacon and pork sticks to expand meat snack offerings to younger consumers. This is an area that fits well with the most recent marketing campaign “Taste What Pork Can Do.” On the supply side, companies are also leveraging hogs’ faster generational turnover compared to cattle, which captures a faster-moving supply chain.

As the top-consumed pork item in the U.S., bacon is a common snack, meal and a long-time complementary item to center-of-plate offerings. Peaking circa-2010, bacon gained a cult-like following, expanding beyond breakfast and sandwich toppings. Bacon has already shown up in the meat snack offerings in convenient ready-to-eat formats, and its future looks bright but is a moderate contender to the top market share holder — beef.

On the poultry side, turkey consumption has declined over the past 20 years, and production is contracting as the industry faces severe disease challenges from Avian Metapneumovirus and Highly Pathogenic Avian Influenza. Though there may be opportunities to reposition turkey as a meat snack rather than just a holiday staple or lunch meat. Similarly, chicken meat snacks, such as chicken sticks, are entering the market, providing consumers with convenient, on-the-go protein options.

Chicken consumption has been a growing category for a couple of decades, and this would be another way for consumers to be able to eat chicken. These items would expand the chicken market to be more of an on-the-go product rather than a meal or snack at home.

Consumer demand for protein is elevated

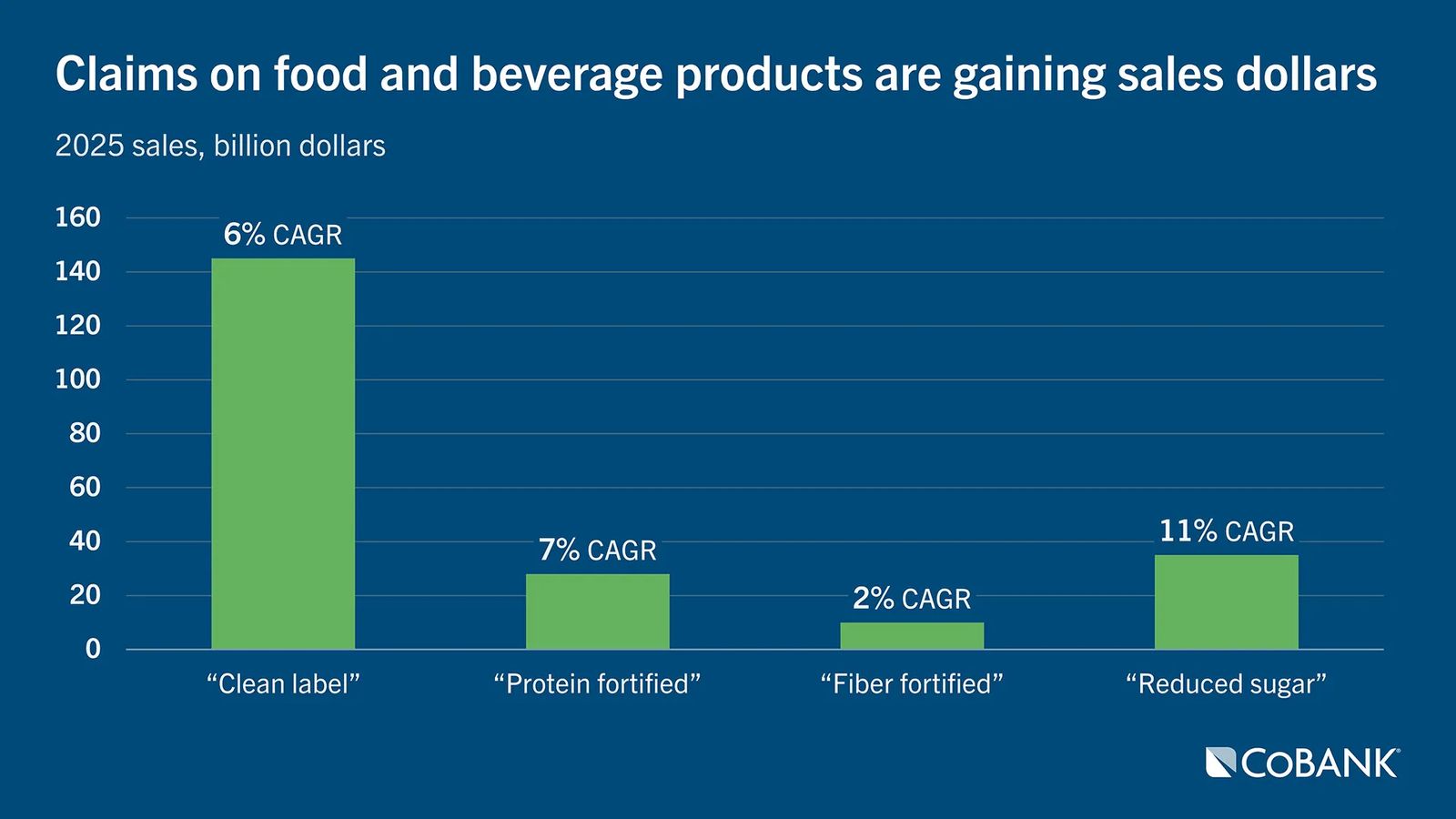

Consumer demand growth today is largely fueled by protein content, nutrient density, clean labels, reduced processing and simple ingredient lists. Shoppers are seeking products that are fresh, healthy and contain fewer additives, with meat snacks often offering single-serving portions, low calories, high protein, negligible sugar and reduced salt — qualities that have driven their popularity over the past year. Meeting these preferences is crucial in today’s food landscape. During 2025, sales of products that claimed protein fortification or a clean label soared over $100 billion, a retail mega-milestone according to recent Ingredion research.

Chipotle has already attempted to get ahead of the expected demand curve with options well positioned to compete directly against beef snacks. Its High Protein Menu includes a snack-sized portion of its chicken and steak offerings. The chain will hardly be the last restaurant group to respond to a challenging 2025 by adapting to GLP-1 driven behaviors and weaker quick-service restaurant traffic.

The U.S. Dietary Guidelines for Americans released earlier this year prioritize protein, meats and dairy, but also advise Americans to minimize highly processed foods. This could present a challenge for some meat snacks. Specifically, it is a very real possibility that regulators or legislators could take a broad approach to defining ultra-processed foods. Government action could prompt manufacturers to reformulate their products to reduce ingredient lists and add healthier elements, namely protein and/or fiber to help “balance” these foods.

Manufacturers of new products in the category have recently responded by explicitly emphasizing simplicity, transparency and fewer ingredients. Jack Link’s is positioning its three‑ingredient meat snacks as made with “honest, simple, minimal‑ingredient products.” Stryve Foods Inc. has repeatedly highlighted “clean ingredients,” “minimally processed protein” and “better‑for‑you snack options” across its recent launches, and New Primal extended its line with “clean protein” and all‑natural poultry snacks. Archer Meat Snacks features clean-label, high-protein and culinary-inspired flavors, and its line grew sales 57.7% in 2025, reportedly on track to exceed $500 million in sales in 2026. The company has also secured a roughly $100 million aggregate credit facility to provide additional capacity to support its growth and expanding national footprint.

GLP-1 is a niche market but has ripple effects

Market dynamics have also been influenced by the rise of GLP-1 weight loss drugs. GLP-1 users lose body mass, often 20% to 25% of their weight, prompting them to seek protein-rich foods to maintain muscle mass while consuming fewer calories.

Meat snacks fit this need, offering health and wellness benefits, simple ingredients, and high protein content in smaller portion sizes. While willingness to pay for premium proteins remains tempered, consumers are gravitating toward smaller, nutrient-dense products like meat snacks. It’s important to note, though, that GLP-1 users represent only about 12% of the population and their use may be cyclical rather than continuous. Household shopping habits are changing as grocery carts cater more to these individuals, presenting both opportunities and challenges for meat snack producers. However, the opportunities outweigh the risks.

Pill forms of GLP-1 weight-loss drugs debuted early this year, promising to be less expensive and simpler than injections, which have been in the U.S. for more than a decade. The expectation is that a pill option will lead to greater adoption of GLP-1 weight loss drugs among American consumers. Citing Research & Markets data, Hormel noted the GLP-1 market is expected to grow from $62 billion in 2026 to $158 billion in 2035.

Households using GLP-1 medications cut spending at grocery stores by 5.3% and at fast-food restaurants by about 8% on average. That’s according to a Cornell Research study published in December 2025 that utilized purchase data from about 150,000 households collected by Numerator. The Cornell study found GLP-1 users are increasing their spending in a handful of categories, including meat snacks and protein bars. Indeed, a February 2026 Fortune headline declared, “Meat snacks have emerged as the clear winner in America’s seismic GLP-1 consumption shift.”

Presuming behavioral shifts hold true for the pill form to take the place of injected GLP-1 drugs, demand for more protein and smaller portion sizes will continue to rise.

The future of meat snacks is bright

Overall, meat snacks represent a significant area for innovation, allowing traditional animal protein companies to become more consumer-centric and differentiate their offerings in a competitive marketplace. The shifting perception of animal processing companies as food brands should help them to connect with consumers and compete more effectively for grocery dollars.

Protein-rich meat snacks have diversified their audience. Per Fortune, Chomps gained 822 basis points of market share over the past three years and, at the same time, grew the traditional meat snack consumer base beyond young males. Chomps notes 70% of its consumers are female, and the potential to grow among new consumers beyond traditional jerky buyers could add sizable growth among families and children. Reflecting that potential, several meat snack companies have expanded their messaging. New Primal is shifting away from “the hypermasculine stereotypes of traditional jerky toward approachable, high-protein solutions for the modern household.”

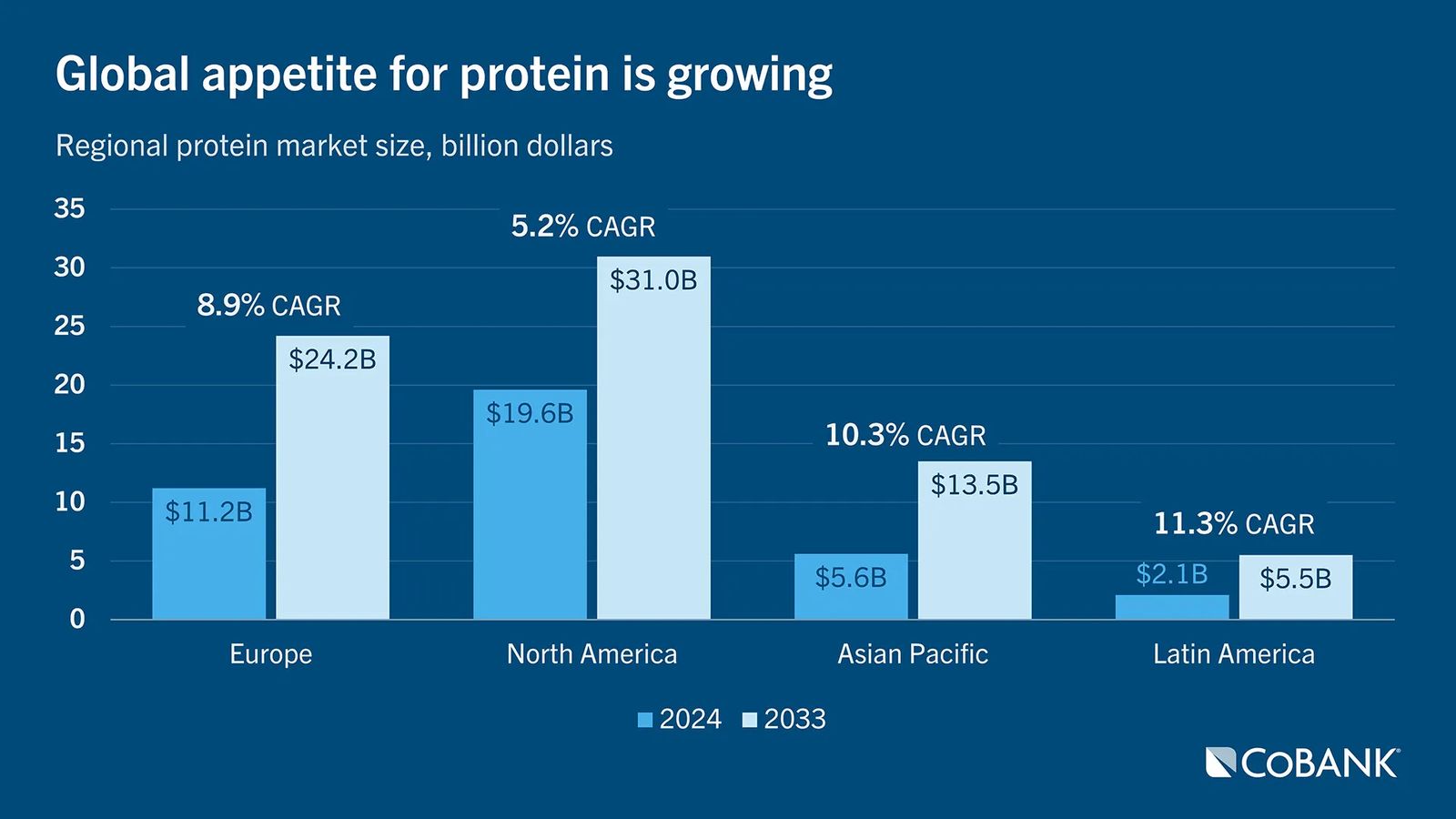

While much of the opportunity is in North America, Hormel notes the potential market is poised to be a global phenomenon. North America currently holds the largest share of dollar sales for protein, yet other areas of the world have a stronger projected compound annual growth rate.

Jack Link’s is focusing on growing share among Gen Alpha, Gen Z and parents with Beast Packs, co-branded with YouTube content creator MrBeast. Meanwhile, Jack Link’s Doritos Nacho Cheese jerky extends a co-branding effort with PepsiCo’s Frito-Lay division that has already seen Doritos Spicy Sweet Chili, Doritos Sweet & Tangy BBQ, and Flamin’ Hot jerky and stick options. Considering the dominant market share of the Doritos brand in tortilla chips (its annual sales of approximately $3 billion represent just under 45% of the market), the launch leans into not only familiar but widely popular flavors of a brand well established with a younger demographic.

In addition to the flavorful partnership with Jack Link’s, PepsiCo has joined the crowded meat snacks category with its own Good Warrior meat sticks. Explaining the rationale behind the launch, a PepsiCo spokesperson noted meat snack consumers are broadening their focus to encompass a greater variety of not only flavors but also premium ingredients, clean labels and such claims as 100% grass-fed beef, in addition to protein content.

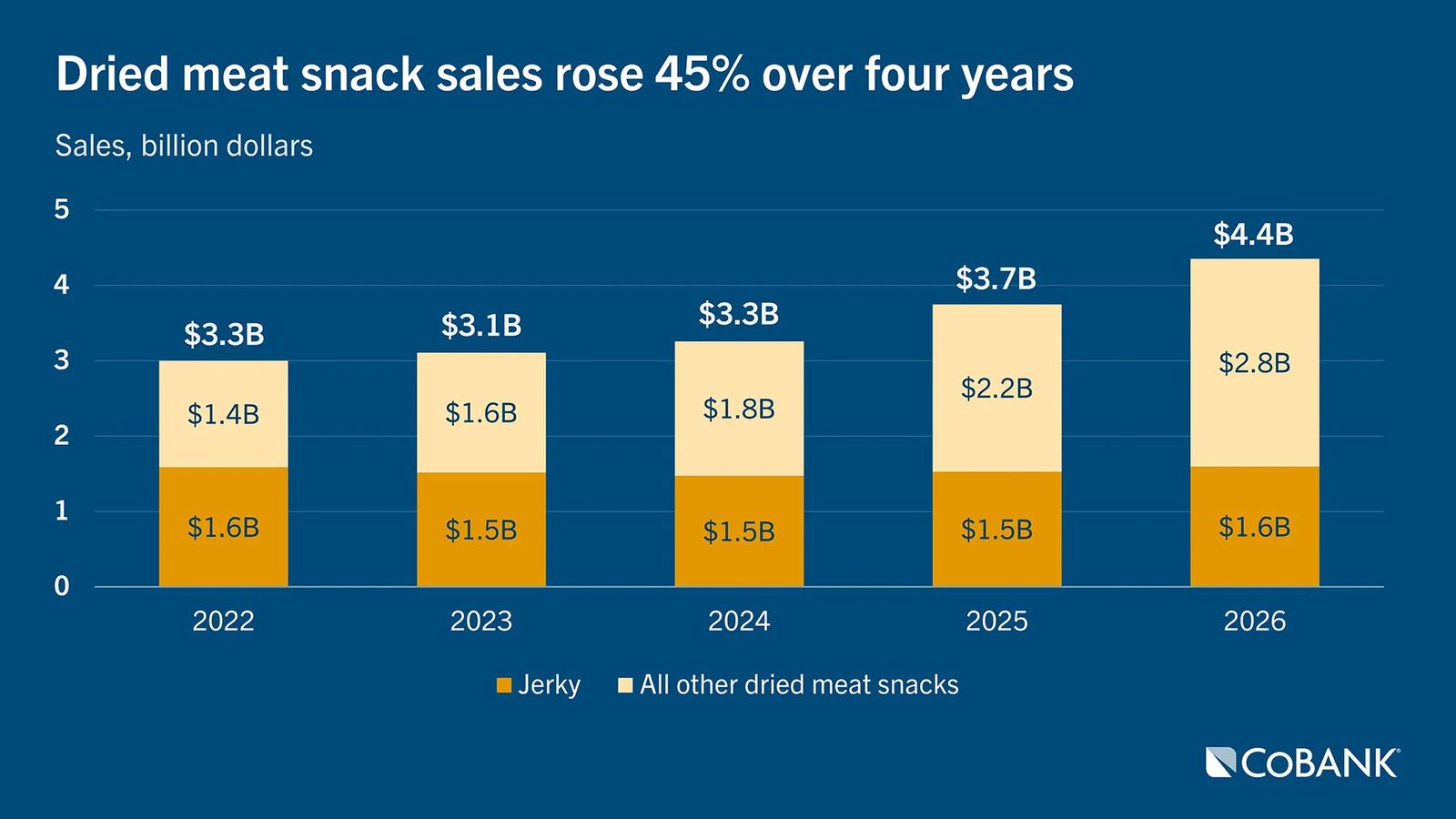

With protein as a top priority for consumers in America and globally, meat snacks are poised to help meet that demand. Circana sales data shows the category has grown by over 45% in the past four years to $4.4 billion, signaling robust consumer investment and likely prompting further investments in processing assets to support future growth While growth in some categories may be tapering, meat snack sales growth is accelerating. Innovation, value proposition, portability and protein importance are all spurring optimism for growth emerging meat snack items alongside other core protein offerings.